On Social Security Reform

We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life, but we have tried to frame a law which will give some measure of protection to the average citizen and to his family against the loss of a job and against poverty–ridden old age.

— Franklin D. Roosevelt (1935)

* * * * *

Social Security is drawn as a “pay-as-you-go” government benefits program. Working people pay a portion of their income to the federal government, and then when they retire, the federal government pays them a monthly benefit.

To fund Social Security, people who are employed pay 6.2% of their wage income as a “payroll tax,” and their employers match this amount. Self-employed people pay the entire 12.4% tax themselves.

The benefit owed to each retiree is based on his highest thirty-five years of income, and is determined by the Social Security Administration with a fairly intricate formula. The benefit amount is adjusted (upward) every year to account for some of the effect of inflation. This is called the cost of living adjustment.

Until 2021, the government collected more money in payroll taxes than it paid out in Social Security benefits. This extra money, or surplus, is held in a trust, and by law, it must be invested in interest earning special issue government securities or publicly traded U.S. Treasury bonds. At this time, the surplus is about $2.8 Trillion.

The United States is in the midst of a demographic shift. As an increasing number of people in the large “baby boom” generation are retiring, a decreasing number of young people are entering the work force and thereby paying into the Social Security system. As things stand, there are not enough people working to fully fund vested Social Security benefits. As a result, in 2021, the government began drawing down the surplus in the trust to meet its benefit obligations.

This demographic problem will continue to worsen, and it is aggravated by the fact that people are living longer. Actuarial estimates are that the surplus will be depleted by 2034. When, i.e., if, this occurs, benefit payments will continue to be made, as the law requires, but the amount of the payments will be based solely on what the then current tax revenues afford. Estimates are that benefit recipients will then suffer a cut of about 23% in their monthly benefit payments.

* * * * *

Assuming that everything else is equal, there are three basic ways to solve the problems attendant to the imminent depletion of the Social Security surplus. Either the payroll tax can be raised, or the benefits can be cut, or the payroll tax can be raised and the benefits can be cut.

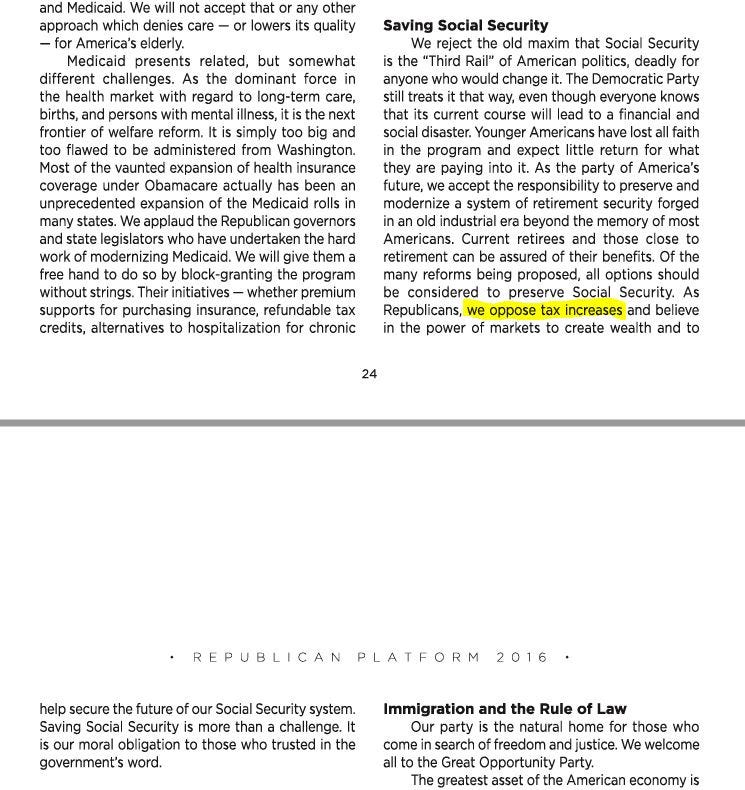

The puppet show in DC is as predictable as it is banal. On the one hand, the Red Team insists that it will not abide a tax increase:

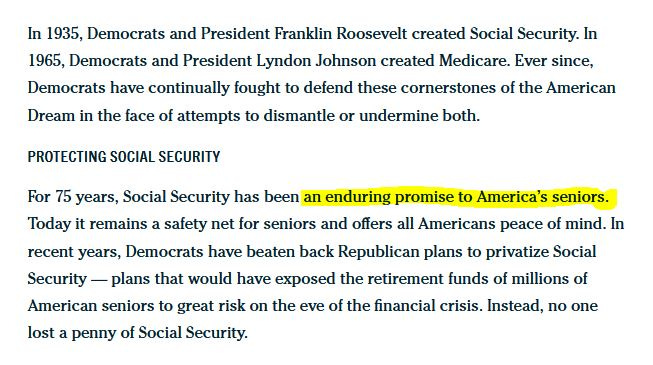

On the other hand, the Blue Team insists that it will not abide a cut in benefits:

Hence, it appears that the problem is intractable. Another example of the politicians being unable to find a bipartisan solution to a bipartisan problem – as if a bipartisan agreement on anything has ever benefited the public. Of course, the government’s dishonesty being pathological, we would be remiss not to consider the possibility that the appearance of intractability is the bipartisan solution. But, I digress.

* * * * *

Background

The Great Depression of the 1930’s created so much social distress that President Roosevelt was able to persuade the Congress to enact the Social Security Act as part of his New Deal. This Act established benefits for old-age retirees, as well as aid for dependent mothers and children, victims of work-related accidents, the blind, and the disabled.

The Social Security Act was signed into law in 1935. The government began collecting the payroll tax in 1937, and began making payments in 1940.

The official name for Social Security is the Old-Age, Survivors, and Disability Insurance Program. The payroll tax revenues are managed by the Social Security Administration, and are held in the Old-Age and Survivors Insurance Trust Fund. This trust fund is an account within the U.S. Treasury, and as noted, the money is invested in special issue government securities and in U.S. Treasury bonds.

At this time, the cost of Social Security benefits is about $1.34 Trillion per year.

This is one of the largest obligations in the annual federal government budget.

Both of these charts are official government charts. I cannot explain the discrepancy between the Social Security budget being $1.34 Trillion, and that sum being 16.1% of the 2023 federal budget. It should be 36%. On the other hand, if the 16.1% is the correct portion of Social Security, the federal budget should be disclosed as $8.32 Trillion instead of $3.7 Trillion. Suffice it to say that Social Security, together with Medicare, is a large percentage of the annual federal budget.

* * * * *

The good news is that even with the demographic changes in the workforce, now and in the foreseeable future, Social Security is not in a terrible place. While the government as a whole is 34% over-budget, Social Security is spending only 8% more than it brings in. To the extent that this is a problem which absolutely, positively must be solved with new legislation, there are several conventional variables on both sides of the ledger.

On the tax increase side of the ledger, proposals include:

1. raising or eliminating the $160,200 limit of wage income subject to the payroll tax,

2. increasing the 12.4% rate of the payroll tax, or

3. broadening the tax base, e.g., to include investment income.

On the benefit cut side of the ledger, proposals include:

1. “means” testing benefits, i.e., indexng benefit payments to need,

2. paying new retirees less than the already retired,

3. reducing the annual cost of living adjustment, or

4. increasing the retirement age.

Not all, if any, of these proposals are politically possible. For example, increasing the payroll tax would hit the lowest income people the hardest. In addition, the public probably could not be convinced to accept a system in which people who are not yet retired will be paid less than the people who are already retired.

Nevertheless, the numbers do not appear to be unworkable. According to the American Academy of Actuaries, if the payroll tax were increased by one percent, and wage income above $400,000 were subject to the tax, while leaving wage income from $160,200 to $400,000 exempt from the tax, then all of the anticipated shortfalls would be covered. Likewise, if the retirement age were raised to 69, and the cost of living adjustment were cut by one percent, this too would cover all of the anticipated shortfalls.

The bottom line is that some combination of a small increase in the payroll tax, imposing the payroll tax on more of the wage income of the upper one percent, a small increase in the retirement age, and small decrease in the cost of living adjustment, would probably solve most of the problems. For example, applying the payroll tax to wage income above $400,000 covers 71% of the expected shortfall, and raising the retirement age to 69 covers 40% of the expected shortfall.

At least mathematically, a solution does not appear to be out of reach.

* * * * *

We are accustomed to thinking of Social Security as a stand-alone program. However, from a “government-wide” perspective, when Social Security reaches insolvency, i.e., when its benefit obligations exceed its payroll tax revenues (and the remaining surplus), not very much will be different. While Social Security does not have the legal right to draw on federal resources to pay the difference between its benefits obligations and its payroll tax revenues, there is no practical reason why the federal government could not continue to make the full earned benefits payments to retirees and other beneficiaries.

There is obvious political power in the ideal of Social Security as a self-financing program in which our citizens, the beneficiaries, earn their benefits through their hard work and contributions. But at the end of the day, this is something of a bookkeeping construction. More importantly, the power inherent in the ideal is not worth the cost of the social devastation which a wanton and wholly unnecessary 23% cut in benefits would likely cause.

I would not have known any of this if not for Steady Rolling. Thank you for keeping me informed.